Over the years Nacha has maintained the ODFI warrants all transactions processed with its routing number. However, on June 30, 2021 the ACH Rules will put a time restriction on breach of warranty claims. So, how long does the ODFI warrant all transactions originated with its routing number?

While the Rules allow RDFIs to return unauthorized entries, they don’t currently address how long the ODFI holds the warranty. Based on state law, the statute of limitations could be two, three or seven-plus years depending on which state’s laws are being followed. To ensure consistency and to align with other payment systems, the ACH Rules will be updated on June 30, 2021 to address limitations on warranty claims.

This change means an RDFI will have a time limit to make a breach of warranty claim against an ODFI for an unauthorized debit its account holder is disputing.

- Non-Consumer Account – An RDFI may make a breach of warranty claim for up to one year from the Settlement Date of the entry.

- Consumer Account – An RDFI is limited to two years from the Settlement Date of the entry PLUS 95 calendar days to make a breach of warranty claim if more than two years has elapsed. The latter timeframe was added to cover cases where the RDFI is still liable to the consumer under Regulation E.

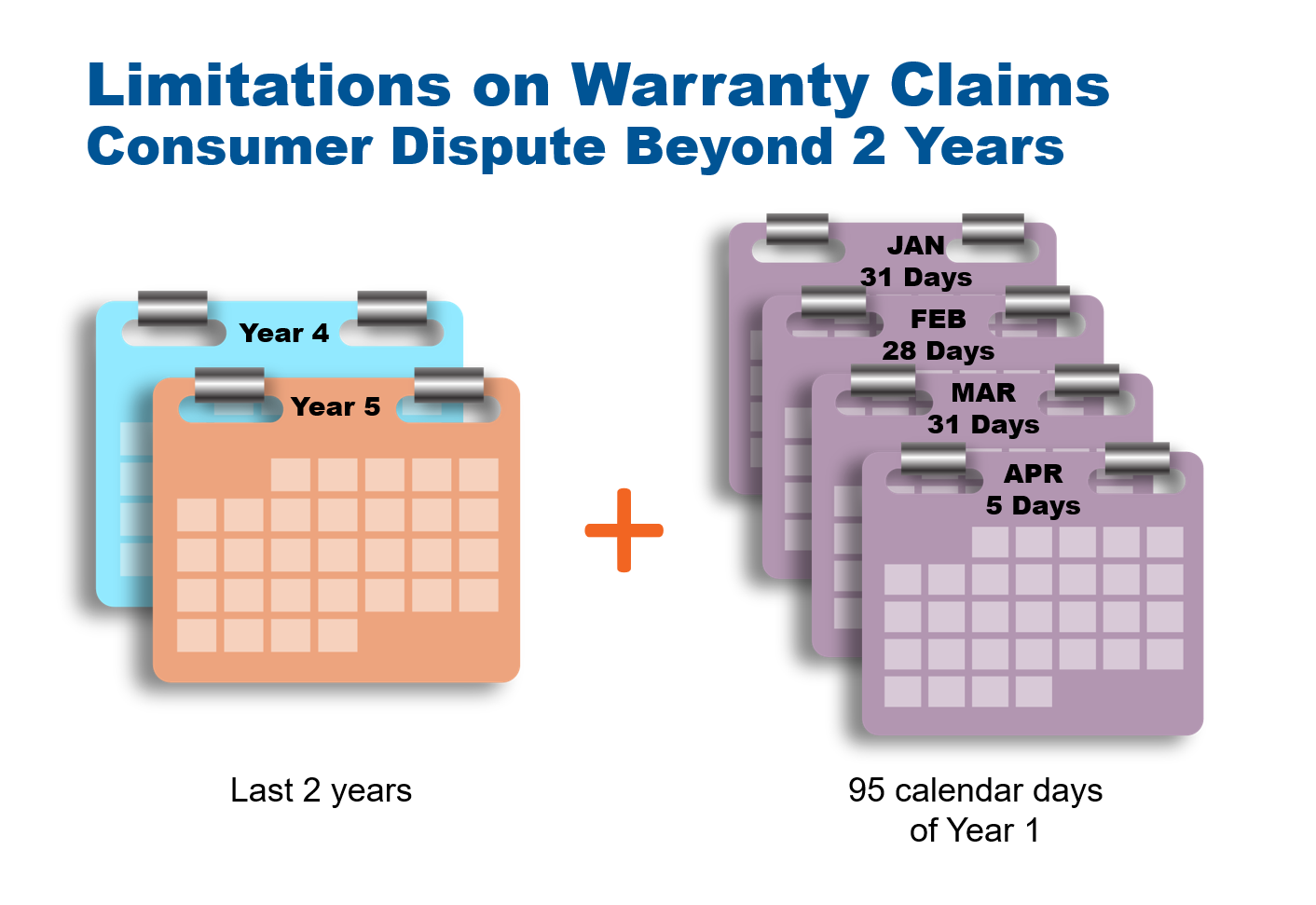

The time limits (one year and two years) are straight forward. But situations where an unauthorized debit is being disputed by a consumer outside of the two-year timeframe aren’t as clear. The time limits (one year and two years) are straight forward. But situations where an unauthorized debit is being disputed by a consumer outside of the two-year timeframe aren’t as clear.

Let’s say a consumer notifies its RDFI of an unauthorized debit that has been taken out of his/her account monthly for the past five years. What is the RDFI’s time limitation on making the warranty claim?

Since the dispute is being made more than two years past the Settlement Date of the unauthorized debit entry, the RDFI can make a breach of warranty claim for the last two years of transactions (years four and five) AND for the first transaction five years ago (year one) plus for transactions within 95 days of that Settlement Date of the first transaction.

With this change, the RDFI should NOT be held liable for any unauthorized transactions as the transactions are covered under the ACH Rules and Regulation E. The ODFI/Originator and the Consumer are liable for certain transactions depending on when the transactions are disputed.

To learn more about this and other upcoming ACH Rules changes, subscribe to our 2021 Payment Systems Update series that will begin streaming via Zoom next month! Your subscription will include ALL THREE of the update’s two-hour series (aka webinars). Multiple offerings of each webinar are available for ease of scheduling, with recordings made available to those who subscribe to the series. Click here for more information about how this year’s streaming will work and subscribe today so you will be ready to binge what you need to know about key changes coming in the year ahead!

Want to Learn More from Karen?

Join us on February 10 for our first Quarterly Compliance and Fraud Review webinar of 2021! During this first update we will cover your annual regulatory education requirements, FinCEN's rule proposal set on virtual currency, pandemic SAR (Suspicious Activity Report) considerations, the Regulation D interim final rule, new ACH Rules, Nacha's latest RFC on Same Day ACH, EIP payments and more. Recent fraud scams, predictions, considerations and mitigation techniques will also be covered. Register now! |